Itemized Business Deductions 2 Floor

What Itemized Deductions Will Look Like In 2018 680 The Fan Wcnn Am

Https Apps Irs Gov App Vita Content Globalmedia Teacher Itemized Deductions Detail Worksheet 4012 Pdf

Standard Deduction Vs Itemizing Yr Tax Compliance Llc

Tax Reform 2018 The Impact On Itemized Deductions For Individuals Jfs Wealth Advisors

Does The Standard Deduction Or Itemizing Make Sense For Your Taxes

The Pros And Cons Of Standard Vs Itemized Tax Deductions

Miscellaneous itemized deductions subject to 2 floor deductions for certain professional fees licenses union etc investment expenses and unreimbursed employee expenses have been suspended.

Itemized business deductions 2 floor.

Itemized Deduction Templates 2 Printable Word Pdf Formats Deduction Templates Words

What You Need To Know About Schedule A White Coat Investor

How The New Tax Law Is Different From Previous Policies Cassaday Company Inc

What Is The Standard Deduction Vs Itemized Deduction H R Block

Part Time Contractor How To Track Your 1099 Expenses

Property Management Forms Templates In 2020 Rental Property Management Property Management Being A Landlord

The Ultimate List Of Itemized Deductions Standard Deduction Deduction Tax Deductions List

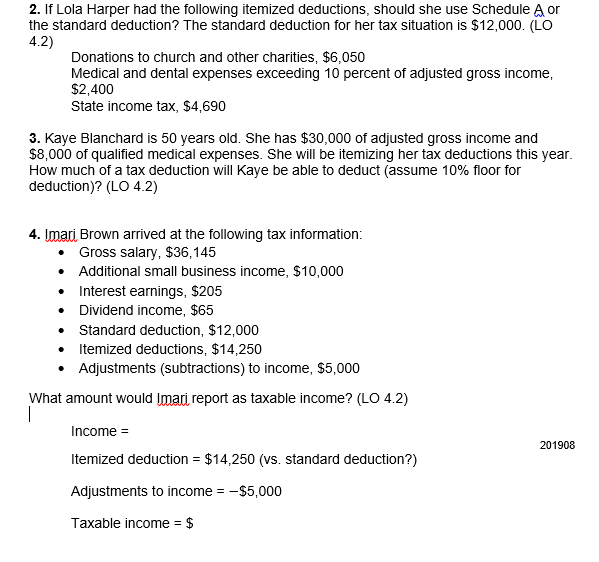

Solved 2 If Lola Harper Had The Following Itemized Deduc Chegg Com

Home Business Magazine Publisher 1080 20191125190656 49 Costco Turbotax Home And Business 2017 The X File In 2020 Home Business Business Account Business Magazine

What The Tax Act Means To Your Schedule A Rbce Inc Taxes And Bookkeeping

Form W 11 Number 11 11 Common Mistakes Everyone Makes In Form W 11 Number 11 Form W 11 Number 11 11 Common Mistakes Everyone Makes In For How To Get Money Irs

Security Deposit Deductions List What Rental Damage Could Cost Rental Property Investment Rental Property Management Real Estate Investing Rental Property

Standard Vs Itemized Deductions

Tax Deductions Get The Nitty Gritty On Which Ones You Can Claim Tax Deductions Deduction Tax Day

Source : pinterest.com